This bloomberg article on gold mining cost is interesting (click link).

Summary of article: gold production has all-in cost of US$1300 in north America. Some gold mining companies like Barricks have US$1100 all-in gold mining cost.

Means it seems difficult for gold to drop significantly below US$1100. below which gold production will be cut significantly and maybe causing supply to drop and price to stabilise or go up eventually. At this moment of rapid gold drop, it is a test in investor's faith in PP strategy. So gold has dropped about -17% since start of this year. Since gold is only about 25% of portfolio, the -17% drop in gold this year will reduce total portfolio by (-17%/4) = -4.25% only, hardly a very big drop to worry about. In comparison, stocks have had typical drops of -40% to -60% during recessions, in which case investor will also have to face the same test in their faith in PP. So as of now, if the rebalancing bands has not been reached for gold, I suppossed investor should not be too worried for PP strategy for now, especially given there may be a logical bottom price for gold. If one is due for rebalancing now, it seems a good time to rebalance into gold, especially if the investor is investing for the long term. As for myself, I have rebalanced into gold last month, so now I will sit on my hand according to strategy and ride through this drop in gold price.

According to A. Gary Shilling's latest book: "The Age of Deleveraging", this decade for U.S. may see U.S. consumers save more and spend less, reducing U.S. imports from emerging countries, and reduce demands for goods from these countries, which is not so good news for emerging countries economy which are mainly export dependent. Therefore Gary forsees continuing weak price pressure, meaning, inflations are not very likely due to increasing U.S. consumer increasing savings, paying back loans and reducing spending, and for other reasons he also mentioned, some U.S. deflations might be more possible in this decade of possible slow growth and deleveraging, despite the massive Quantitative Easing by the U.S. government.

Given the prospect for the strengthening Singapore dollar which is slight negative for gold in SGD, and the prospect of US deflations which is negative for gold, and the prospect for low global growth in this decade, I am not so optimistic for gold price in SGD in near term if there is no major global financial crisis. However, gold is still necessary to hold in portfolio as insurance against inflations or monetary devaluations. Also, I do not know how the future will unfold, therefore i am not in a position to market time with gold or other assets right now, hence sticking with the PP strategy seems the better choice now, especially given PP's past track records.

In the future, when people start to take action against inflations, such as stocking much more inventories than they currently need, in order to save money in expectation of higher future prices and inflations, then that is a sign and I will look at gold more closely because such excessive stocking activities are one of the main cause of the past high inflations in US in 1970s, which had caused gold price to soar.

Thursday, 18 April 2013

Monday, 10 December 2012

Being a Passive Portfolio Investor

Every now and then, I wonder if I should optimise my portfolio allocation in order to maximise my potential returns to my passive portfolio. The smart move will be to 'dumb' my mind and stop my thought immediately about changing portfolio allocation. These articles extracts show some reasons to remind myself to 'dumb' my mind about active investing and just let the passive investing strategy do its work. The 3 reasons are as follows:

1. It is fine to only capture a great part of the gains offered by volatile market.

A tempting variation on the passive investing strategy is the macroeconomic trend idea. In simple terms, an investor who would otherwise pursue a completely passive investing strategy seeks instead to “play macro.” He or she attempts to guess the direction of an economy over the next several quarters and invests accordingly.

It’s tempting, compared to a true passive investing strategy, because financial charting software makes it very easy to create flattering views of one’s own opinions.

Think gold is done? You can get a chart to prove it in two clicks. Interested in Brazil? No problem. Run a quick search on the country’s major stock index and, voilà, there’s your case for investing today.

The difficulty, of course, is that global economies are very complex machines with many moving parts. There’s no good reason gold can’t bust higher and higher, testing your will to sell. A minor change in Chinese growth could hammer Brazilian exports overnight. Your passive investing strategy turned semi-active would wipe out fast.

......

Hindsight is always perfect in these situations. Buying the Dow in March 2009 would have been a brilliant play, but only if you managed to sell the Dow as it peaked in October 2007. A passive investing strategy, of course, would not have taken these actions so bluntly.

A more productive approach, then, is to abandon the idea that macroeconomic analysis is within your grasp as an ordinary human being. It’s an interesting hobby and great background for your intellectual life, but not a bet to take with your retirement funds.

A true passive investing strategy nevertheless offers ways to capture a great part of the gains offered by volatile markets without taking “all-in” bets based on limited information.

......

A simple ETF- and index fund-based passive investing strategy allows you to play these macro waves with confidence, and you needn’t be right about anything at all, just disciplined about rebalancing when the opportunity arises.

Source: http://www.marketriders.com/investing/passive-investing-strategy-that-works/

2. I do not claim to be as 'intelligent' as these people to decide accurately when i can do active investing, and when i can do passive investing.

Deciding when to use the optimal approach

At the core of our active investment process is an understanding of the influence of the behavioural aspects of markets:

As the market’s long-term growth trend re-emerges, we advocate returning to a more passive investment strategy which focuses on capturing the rising tide of the markets.

3. Remembering permanent portfolio's lower potential drawdowns can also help calm my mind and allow me to let my portfolio sit through market turmoils as designed.

There's a strong tendency for many in the financial media to overcomplicate this thought process-and I'm not necessarily knocking. There's a big difference between earning 7% on $100,000 for 30 years compared to earning 8%. One will get you $800,000 and the other will get you about $1.1 million.

......

But for me, that difference is dwarfed by the necessity to avoid selling out at the bottom - the avoidance of selling is the dividend investor's key to success. If you can craft a strategy that holds through fear and panic, you've won. You did it. You've conquered the biggest demon of the capitalist markets. That's the big point of dividend-growth investing: the growing income checks during periods of economic turmoil provide a comfortable measurement that prevents investors from irrationally selling out at a market low. That's the secret sauce.

Source: http://seekingalpha.com/article/1052891-the-greatest-benefit-of-dividend-growth-investing

1. It is fine to only capture a great part of the gains offered by volatile market.

A tempting variation on the passive investing strategy is the macroeconomic trend idea. In simple terms, an investor who would otherwise pursue a completely passive investing strategy seeks instead to “play macro.” He or she attempts to guess the direction of an economy over the next several quarters and invests accordingly.

It’s tempting, compared to a true passive investing strategy, because financial charting software makes it very easy to create flattering views of one’s own opinions.

Think gold is done? You can get a chart to prove it in two clicks. Interested in Brazil? No problem. Run a quick search on the country’s major stock index and, voilà, there’s your case for investing today.

The difficulty, of course, is that global economies are very complex machines with many moving parts. There’s no good reason gold can’t bust higher and higher, testing your will to sell. A minor change in Chinese growth could hammer Brazilian exports overnight. Your passive investing strategy turned semi-active would wipe out fast.

......

Hindsight is always perfect in these situations. Buying the Dow in March 2009 would have been a brilliant play, but only if you managed to sell the Dow as it peaked in October 2007. A passive investing strategy, of course, would not have taken these actions so bluntly.

A more productive approach, then, is to abandon the idea that macroeconomic analysis is within your grasp as an ordinary human being. It’s an interesting hobby and great background for your intellectual life, but not a bet to take with your retirement funds.

A true passive investing strategy nevertheless offers ways to capture a great part of the gains offered by volatile markets without taking “all-in” bets based on limited information.

......

A simple ETF- and index fund-based passive investing strategy allows you to play these macro waves with confidence, and you needn’t be right about anything at all, just disciplined about rebalancing when the opportunity arises.

Source: http://www.marketriders.com/investing/passive-investing-strategy-that-works/

2. I do not claim to be as 'intelligent' as these people to decide accurately when i can do active investing, and when i can do passive investing.

Deciding when to use the optimal approach

We believe certain times call for a passive investment strategy, whereas in other times an active approach is more prudent.

In the 1980s and 1990s, the market rose steadily for two decades, partially as a result of:

- Falling interest rates

- Baby Boomers entering the workforce and their prime spending years

- Globalization, which helped keep the cost of living low, as goods were made cheaply overseas.

- The advent of the Internet Age

During this time, a prudent investment strategy was to be passively invested in the market using a “buy-and-hold” approach with minimal trading, and through low-cost investment vehicles.

- At times of extreme investor exuberance, risky assets are priced for perfection and we are then encouraged to reduce our exposure to them.

- Conversely, extreme investor fear leads to assets being priced at “fire sale” valuations and we are encouraged to prudently purchase quality assets at “cheap” levels.

As the market’s long-term growth trend re-emerges, we advocate returning to a more passive investment strategy which focuses on capturing the rising tide of the markets.

3. Remembering permanent portfolio's lower potential drawdowns can also help calm my mind and allow me to let my portfolio sit through market turmoils as designed.

There's a strong tendency for many in the financial media to overcomplicate this thought process-and I'm not necessarily knocking. There's a big difference between earning 7% on $100,000 for 30 years compared to earning 8%. One will get you $800,000 and the other will get you about $1.1 million.

......

But for me, that difference is dwarfed by the necessity to avoid selling out at the bottom - the avoidance of selling is the dividend investor's key to success. If you can craft a strategy that holds through fear and panic, you've won. You did it. You've conquered the biggest demon of the capitalist markets. That's the big point of dividend-growth investing: the growing income checks during periods of economic turmoil provide a comfortable measurement that prevents investors from irrationally selling out at a market low. That's the secret sauce.

Source: http://seekingalpha.com/article/1052891-the-greatest-benefit-of-dividend-growth-investing

Wednesday, 24 October 2012

STI Review 2012 Oct and Guide 3 to Investing Plan A and Plan B

Here is the third action plan continued from previous two posts.

3. Plan B: What to do with existing stock

portfolio now if market is really 'not cheap'?

An investor has to choose a suitable

Plan B plan for market downturns, else risk losing all the 'paper profits' or

worse, incur losses. Capital protection is as important as capital appreciation

and income in investments. There is no point to grow a 100k portfolio by 100%

to 200k, only to have a major market downturn decrease portfolio by 50% and

make the 200k back to square one 100k again, or worse. Capital loss can be made back, but

the time and years that were used to get the 100% gain will be wasted and the

time cannot be recovered. Having Plan B is especially important for a

pure equity investor as such pure equity portfolio is very volatile, and equities can lose a lot quickly in

times of stock market distress. Wiht a suitable plan B, the investor can keep calm instead of panicking

and doing disastrous things to portfolio. For a bond and stock passive

portfolio investor, Plan B is already built into portfolio through mechanical

rebalancing and having the negative correlation between stocks and bonds, so passive portfolio investor just ride the ups and down more calmly.

So in summary, Plan A is for new investor to decide when and how to start a portfolio in order to start investing on a firm foundation. Plan B is for investor to decide how to preserve capital and retain profits. There is another Plan C which is to decide how to drawdown the money from a portfolio at a sustainable rate during retirement so the drawdown can last for a lifetime, and so Plan C is another topic to be discussed separately.

3. Plan B: What to do with existing stock

portfolio now if market is really 'not cheap'?

This section is more for newer

investors who may not have made suitable contingency plan B for market downturns.

So what has been your plan B when stock market is not going for a downturn?

Basically there are 5 possible kinds of plan B.

First kind of plan B is to hold on

to stocks and hoping the market goes up, up, up, and never come down, while

having no clear idea when to sell to lock in profit - this is just pure gambling,

not investing. In investing there is no hoping. Investing follows a clear plan

regarding when to enter or exit positions and rebalance assets in different

possible market conditions. So better start adopting one of the next few plans

now.

Second kind of plan B is to sell off

some stock to lock in capital gains profit when warning signs of market turning

are apparent, then to hold some cash and ride the market down with rest of

stock assets, and wait till market bottomed adn turn upwards to buy back cheap stock

with cash. This way, in case the market downturn is a very short one, there

will still be stocks to take advantage of the next leg up in stock prices. In my opinion, it

is more correct to say a pure equity portfolio has 2 kinds of assets – stocks and

cash savings. It may be 90% stock and 10% cash savings now. If a major market

downturn is expected, an investor may wish to sell some stocks and leave the

defensive stocks, so that stocks become 50%, cash savings become 50%. The 50%

cash will create buffer to reduce overall portfolio loss. The 50% stock is in

case the stock market keeps on going up, which is why one may need to always be

invested in market. Seeing a stock portfolio as 2 assets and in terms of percentages

can make it easier and more mechanical to do such profit taking and

rebalancing.

Third kind of plan B is to sell off

part of stock portfolio and buy some government bonds to buffer and reduce

potential stock losses, before downturns happen. For a pure equity portfolio,

this will be selling some equity to take some profit and diversifying into bond

to reduce the portfolio risk. If one already has a bond and stock portfolio,

this is just normal rebalancing and profit taking. For a current pure equity

portfolio, switching partly into bonds also allows profiting from the

appreciating bond prices so that at suspected market bottom, the appreciated

bond price can be sold to buy more cheap stocks. Another advantage is that

since portfolio losses are smaller, when cheap stocks are bought and the market

recovers, the losses are recovered more quickly and portfolio can also get

bigger gains.

Fourth kind of plan B is to sell off

entire portfolio at suspected market top and call it a good run. This is market

timing and this game plan is not suitable for most people, since it takes

unique skill to market time correctly and consistently and one has to be sure

one has the correct psychology to really be able to let go and sell everything

when the telltale warning signs appear in market. The bad part is if the

investor mind is not strong enough and has no clear exit strategy, it then

became a gamble. So if the market downturns suddenly, and the investor keep

waiting for price to retrace back up before selling, and when price retrace

back up a little, wait some more for price to rise only to find that the price

keep dropping and dropping already, until investor panic and sell at small

profit, to break even and forfeit profits, or even incur losses.

The fifth and last but not least plan

B is to buy value stocks or dividend stocks and do not sell them ever, unless

under specific circumstances. This is the Warren Buffet plan B and we all know

how successful he is at value stock picking. and growing portfolio If one has the Midas touch and is

successful at stock picking of value companies and business, then this is the

way. Otherwise for typical investors who do not have this magic touch of

picking correct value stocks, this buy and forever hold approach is not

suitable.

So in summary, Plan A is for new investor to decide when and how to start a portfolio in order to start investing on a firm foundation. Plan B is for investor to decide how to preserve capital and retain profits. There is another Plan C which is to decide how to drawdown the money from a portfolio at a sustainable rate during retirement so the drawdown can last for a lifetime, and so Plan C is another topic to be discussed separately.

My view on STI is not a market

prediction to sell now, it is just the warning signs as I see it, and your

investment decision should not be based on my input alone. Rather, I am using

this example to point out possible good and bad entry strategies for potential new

stock investors so that they can avoid costly entry mistakes, and to get new

and existing investors thinking about having a strategic game plan B to

preserve investment capital during future market downturns. If my views on STI

prove true in next few months, then hopefully more investors will be prepared

to weather downturns well. If my views are absolutely wrong in next few months and

STI rose like nobody’s business, then new investor can still take heed to formulate

a strategic plan B so that new profits can be kept in future downturns. Good

luck and good investing to all.

Disclaimer: I am not a financial adviser and I am not

working in finance related industry. I am an investor for my own assets and

speaking from my personal viewpoints. Readers should do their own due diligence

and learn about any investing strategy and suggestions well before using them.

I will take no responsibility for your investment results. I am currently vested

in 4 assets, namely SPDR STI ETF (ES3), 30-year Singapore Government Bond

(PH1S), Gold ETF (O87), and my own cash savings.

---------------------------------------------------------------------

Go to:

Part 1 of Article - Guide 1 to Investing Plan A and Plan B

Part 2 of Article - Guide 2 to Investing Plan A and Plan B

---------------------------------------------------------------------

Go to:

Part 1 of Article - Guide 1 to Investing Plan A and Plan B

Part 2 of Article - Guide 2 to Investing Plan A and Plan B

STI Review 2012 Oct and Guide 2 to Investing Plan A and Plan B

Here is the second action plan continued from previous post.

2. Another Plan A: Enter a 'not cheap' market now

with a diversified portfolio.

What if you don't want to risk

missing the boat and for some reason you have to start investing now, even when

the market is 'not cheap'?

I know the feeling, been there myself also. When I started my diversified passive portfolio, no time seems like a good time to start - when there is a cheap asset, there may also be an expensive asset. The best time to start a portfolio is at the bottom of a recession, when many investment assets are very cheap and people are staying away from these assets like they are smelly tofu. I'll say the smellier the smelly tofu, the better it is eat. So learn to eat smelly tofu already...haha.

That said, I think only experienced investor will have the guts and know-how to start investing at market bottoms. So back to the question of new investor, what to start investing in when market is 'not cheap'. In my opinion, when stock market is 'not cheap', it is better to start a diversified portfolio.

By diversified I mean besides buying stocks, buy also Singapore government bonds. The way it works is government bonds price will move in opposite direction to stock market price. If stocks are 'expected to rise' for long period, bonds price will drop as people leave bonds to chase better returns in stocks. On the contrary, if stock prices are 'expected to fall for long period', people will drop stocks and run to bonds for the relatively safer and consistent yield.

Now if you have both stocks and bonds when market is 'not cheap' this is what is going to happen usually. If bet correctly and stock market goes up, stock price will normally rise faster than bond price drop, hence you will still make a net profit. If bet incorrectly and stock price drops, bond price will rise and offset some or most of the big drop in stock prices, therefore your net loss will be lesser than the average stock market loss, hence making your lesser loss more bearable. At the bottom turning point of market, or when stock price has been at or below 200MA for a long while and there may be price divergence with MACD again, perhaps that will be a good time to sell off some or most of your profitable bonds and buy into cheaper stocks.

This way, if you win you won’t win too much but at least as a new investor in a 'not cheap' market, having some win is better than facing potential big loss. If you lose, it will be more bearable as your total loss is lower compared to the average stock market loss, and you may also take some comfort at watching how the bond keep growing when stock prices are dropping. And even if you lose, you will still have a 2nd chance to sell the profiting bonds to buy cheap stocks later on, hence making back the loss faster than if you were to buy only stocks at possible height of market.

Having a diversified stock and bond portfolio is a way to reduce 'volatility' in a portfolio, meaning reducing the potential loss (and gain) in a portfolio. Avoiding big loss is important for new investors so that new investor will not panic, cut loss, and throw away the investment strategy. A diversified stock bond portfolio, rebalanced yearly, has practically the same returns as a stock index portfolio over the long run, so stock/bond portfolio is not missing out on much while enjoying lower volatility. So how to start a stock bond portfolio? There are 3 things to decide: asset allocation ratio, which particular stock to buy, and time to rebalance.

2. Another Plan A: Enter a 'not cheap' market now

with a diversified portfolio.

What if you don't want to risk

missing the boat and for some reason you have to start investing now, even when

the market is 'not cheap'?I know the feeling, been there myself also. When I started my diversified passive portfolio, no time seems like a good time to start - when there is a cheap asset, there may also be an expensive asset. The best time to start a portfolio is at the bottom of a recession, when many investment assets are very cheap and people are staying away from these assets like they are smelly tofu. I'll say the smellier the smelly tofu, the better it is eat. So learn to eat smelly tofu already...haha.

That said, I think only experienced investor will have the guts and know-how to start investing at market bottoms. So back to the question of new investor, what to start investing in when market is 'not cheap'. In my opinion, when stock market is 'not cheap', it is better to start a diversified portfolio.

By diversified I mean besides buying stocks, buy also Singapore government bonds. The way it works is government bonds price will move in opposite direction to stock market price. If stocks are 'expected to rise' for long period, bonds price will drop as people leave bonds to chase better returns in stocks. On the contrary, if stock prices are 'expected to fall for long period', people will drop stocks and run to bonds for the relatively safer and consistent yield.

Now if you have both stocks and bonds when market is 'not cheap' this is what is going to happen usually. If bet correctly and stock market goes up, stock price will normally rise faster than bond price drop, hence you will still make a net profit. If bet incorrectly and stock price drops, bond price will rise and offset some or most of the big drop in stock prices, therefore your net loss will be lesser than the average stock market loss, hence making your lesser loss more bearable. At the bottom turning point of market, or when stock price has been at or below 200MA for a long while and there may be price divergence with MACD again, perhaps that will be a good time to sell off some or most of your profitable bonds and buy into cheaper stocks.

This way, if you win you won’t win too much but at least as a new investor in a 'not cheap' market, having some win is better than facing potential big loss. If you lose, it will be more bearable as your total loss is lower compared to the average stock market loss, and you may also take some comfort at watching how the bond keep growing when stock prices are dropping. And even if you lose, you will still have a 2nd chance to sell the profiting bonds to buy cheap stocks later on, hence making back the loss faster than if you were to buy only stocks at possible height of market.

Having a diversified stock and bond portfolio is a way to reduce 'volatility' in a portfolio, meaning reducing the potential loss (and gain) in a portfolio. Avoiding big loss is important for new investors so that new investor will not panic, cut loss, and throw away the investment strategy. A diversified stock bond portfolio, rebalanced yearly, has practically the same returns as a stock index portfolio over the long run, so stock/bond portfolio is not missing out on much while enjoying lower volatility. So how to start a stock bond portfolio? There are 3 things to decide: asset allocation ratio, which particular stock to buy, and time to rebalance.

First thing, about allocation

ratio. If you are conservative investor who do not like large losses, use 50%

stock and 50% bond, which will offer lesser potential loss and more stable

portfolio returns. If you are young and aggressive investor, or with high

stream of future cash income, use 70% stock and 30% bonds (or 80% stock and 20%

bond if you have very high stream of cash income), which will offer more stock

returns and also potentially higher stock loss - higher stock loss may be

alright if you have future high streams of cash income which allows you to

average down on stock all the while when the market is falling.

Second thing, about what particular

assets to buy. For bonds, I would say get 30 year Singapore Government Bond

only. Choosing only local bond to avoid currency risk. Choosing government bond

instead of municipal and corporate bonds to avoid default risk during bad

economic times, and Singapore Government bond is rated AAA, so why not? Choosing 30 year

long bonds instead of 10 year medium bonds or 2 year short bonds, because 30

year bonds is more volatile than short or mid-term bonds. In recession, higher

volatility of 30 year long bond will allow this bond price to spike up more and

greatly offset potential drops in stock price. If stock goes up instead, this

long bond will drop faster also than short or medium term bonds. This is ok

because normally, historically and practically speaking, stocks will rise

faster than drops in this bond, which will still allow net profits for stock

bond portfolio. About interest rate risk for bonds, long term 30 year bond price are also

negatively affected by rising interest rate, more so than short term adn mid term bonds. In the next couple of years, I do

not foresee risk of rise of interest rate, since U.S. central bank is committed

to maintaining interest rate low till 2015 and Singapore government will likely

follow suit. The European situation will also take some more years to resolve till it does not negatively impact on global economy.. Even if interest rates rise in future, if you are a long term

diversified portfolio investor, it will still be good to be consistent and hold

on to 30year long bond for the long term volatility protection. Consistent strategy is key for diversified portfolio investing.

Third thing, what is rebalancing and

when to do it. If you invest in such stock bond portfolio for long term, then

some time after you start the portfolio, stock and bond prices will change and

the stock bond allocation ratio will change accordingly. Let's say after one

year, a 50/50 stock bond portfolio becomes 60/40, meaning stock has had a good

run and overtake bond price drop. So at end of the year, sell stock to buy

bonds, or top up with fresh cash on new bonds, to get back to 50/50 allocation.

In this way, you are forcing yourself to mechanically sell for profits and buy

assets when they are cheap. This is called rebalancing, and is preferably done

every year, or sometimes every quarter or even month, depending on the optimal commission

costs and availability of fresh funds. You may say you are missing out on stock profit by selling stocks every year, but if there is a sudden stock market correction, teh 50% bonds is there to ensure you keep most of your profits instead of throwing profits back to the market.

If you are looking to implement a

more diversified long term portfolio now or in future, you can check out the

Permanent Portfolio passive investing strategy which holds stock index fund,

government long bond, gold and cash. Permanent Portfolio is an unconventional strategy offering even lower volability while offering similar long term returns to sotck index fund.There are also other mroe conventional passive portfolio

strategies available too under different names. Also, stock and bond portfolio

like this are not unique, it is the basic building block of many fund managers

and their diversified investment and retirement funds. So you can also choose

to maintain a simple diversified passive portfolio for yourself one day if your investment needs change and you become more risk adverse.

Continue to read Part 3 using below link.

---------------------------------------------------------------------

Go to:

Part 1 of Article - Guide 1 to Investing Plan A and Plan B

Part 3 of Article - Guide 3 to Investing Plan A and Plan B

Continue to read Part 3 using below link.

---------------------------------------------------------------------

Go to:

Part 1 of Article - Guide 1 to Investing Plan A and Plan B

Part 3 of Article - Guide 3 to Investing Plan A and Plan B

STI Review 2012 Oct and Guide 1 to Investing Plan A and Plan B

Singapore STI Review 2012 Oct and Guide 1 to Investing Plan A and Plan B

Here is my view on current Singapore Straits Times Index. First see the current STI chart:

STI is making newer one year price

high this year. Is now a good time to start your new stock portfolio or buy new

units to ensure you get into action for a possible next leg up in stock market?

There are a few warning signs against doing so now:

1. The STI is way above 200 days

moving average now. When the price is way above 200 MA, in my opinion this is a

gauge that the price is definitely not cheap to buy.

2. There is a price divergence

between the higher high in price and the lower high in MACD indicator, see the

orange lines. This usually points to 2 things:

a. The uptrend momentum of STI has

weakened and a possible reversal downwards of price may be coming.

b. The uptrend momentum is still

strong and price will keep making newer high and MACD will keep making lower

high.

c. Price is consolidating and ranging horizontally, before price keeps making newer high and MACD will keep making lower high.

Looking at price movement, there is

no way I can say the uptrend is quite strong; at most what I see is a weak

uptrend. So without strong price uptrend, possibility b. seems less probable.

We are left with possibility a. which means uptrend momentum has really

weakened and we are in for a possible downturn in STI. A market downturn can

come silently without warning, and by the time investor is convinced market is

in downturn, they can already be faced with losses and some may be clueless

what to do. Market downturn can also be a good thing for investors who are

prepared to pick up cheaper stock later when market is near the bottom. We are also left with possibility c. which is not so bad as price may be consolidating to go higher. If price is consolidating now, in my opinion there is no need to hurry to buy yet, just wait for price to be at the 200MA before entering, to reduce risk.

Currently I also hear people talking

about how the market is not cheap right now, if so there will eventually be fewer

buyers than sellers and the market may have to take a break and reverse

downwards, in a so called technical market correction. Also, I keep hearing

people talking about how profitable Singapore Reits are and also how not cheap it is

now. Some people even start suggesting to just jump into buying S-Reits without

needing to think - I disagree. Let's look at a quote from 'An investor's guide

to famous last words":

"You can't afford not to own

this stock." - As close as it gets to ringing a

warning bell at the top of a bubble. So start be alert for people who are

saying these 'last words', so called because this will be the last thing we will hear them say before the market turns down and prove them very wrong.

Are we at a turning point in STI soon? Fundamentally there is not much growth engines in the global

economy to support good growth in Singapore economy, and just recently, we were lucky

to have been told we avoided a technical recession. The U.S fiscal cliff is

approaching, so current uncertainties faced by U.S. businesses is not good

for business growth. Think of how uncertain the market was during the episode

last year when U.S. politicians were haggling over raising the debt ceiling, and

how the stock market rapidly dropped during that period from August 2011 onwards. Now after

the U.S. election on Nov 6 2012, the market may also make a correction. Another

thing is the market may act strange also when Dec 21 2012, the end of Mayan calendar,

is approaching... maybe this is a myth, well, like the Y2K event, we will have

to see whether this particular period will be a non-event or not.

With the not so cheery view above,

what can I conclude? First, I am not claiming to be a financial guru and I am

not claiming to make prediction that the STI is going to reverse. I just sharing

my views on the warning signs and offering few personal viewpoints here regarding

what to do or what not to do now. I see 3 broad action plans now:

1. Wait for lower price to enter

into stock market.

2. Enter a 'not cheap' market now

with a diversified portfolio.

3. What to do with existing stock

portfolio now if market is really 'not cheap'?

Here are the broad action plans.

1. Plan A: Wait for lower price to enter

into stock market.

For new stock investor, now is 'not

cheap' to start buying into stock market. Price moving above the red 200MA

lines means there was a good run behind the current price, so when you buy into

stock market now, people may be already selling for profits. A better entry point may be

when the STI turns back down and touch the 200MA line, which means there has

been profit taking and price has become average. Another good entry point will

be when price is below the 200MA line for some time, when stocks have become

relatively cheaper and maybe undervalued. For good entry point at or below

200MA, new investor will have to figure out for themselves.

All I am saying is,

if you start buying into stock market now, there is little headroom left to

support much price appreciation. Then if price eventually turns down and you

are caught with negative profits in your portfolio, what are you going to do?

Average down and hope to breakeven someday... while worrying how much more is

the drop?

Investing is about planning, not about hoping. It seems a better way

to just wait for market corrections, which will probably happen once or twice a

year at least. Then when market corrections happens, pinch your nose and buy cheaper stocks

at 200MA and if price drop further below 200MA, be contrarian and average down

- pick somewhere after market bottom up then pinch your nose again and buy into stocks again when people are avoiding stocks as if they were smelly tofu. When you buy stocks cheap, you are actually lowering your risk a lot since there is already lesser room for the stock price to fall compared to if you buy stocks at the top above 200 days MA.

Waiting for a lower better entry

price to buy cheap is better than potentially watching your stocks plunge from

high and averaging down. I have been down this road before, buying pure equity

portfolio at 'not cheap' level when price was way above 200MA, price drop and I

average down, price drop and I have no more money to average down. Price drop

till I cannot tolerate it, cut loss and conclude I did not have a good

strategy. I was not a good market timer back then and knew much less about how

market works than now. Now my investment strategy does not require market

timing, and through learning about the Permanent Portfolio, I also learn more about how the stock and other asset market works.

Continue to read Part 2 using below link.

---------------------------------------------------------------------

Go to:

Part 2 of Article - Guide 2 to Investing Plan A and Plan B

Part 3 of Article - Guide 3 to Investing Plan A and Plan B

Saturday, 20 October 2012

The Reasons for Using Passive Investing Strategy

My

Passive Investing Portfolio

Both my cash and CPF are invested

into passively managed portfolio using Permanent Portfolio strategy. I am able

to justify investing with passive portfolio because i have studied this

strategy in depth, though about the potential good and bad points, and conclude

the risk reward of this portfolio is suitable for my investment aim: preserve

capital, reasonable growth, no need for market timng, stock picking and company

research, and no need for constant monitoring. The final aim is to grow my

investments into the millions to secure my retirement. Having financial

security and independence along the way will be nice too.

My CPF portfolio is 30% STI ETF, 30%

30-year S'pore Govt. Bond, 30% CPF Cash, 10% Gold ETF, to be rebalanced yearly

- all bought at once using multiple brokerage in April this year. Total returns

including cash interest, for last 6 months, is about 4.25%, not bad for half

year of doing nothing. My cash Permanent Portfolio portfolio started off from

February to April this year with 25% equal split of STI ETF, UOB Gold savings

account, 30-year Singapore Government Bond, and cash, and is having similar

returns as the CPF portfolio now. This is not a bad start for me, as being able

to make some significant profits without me having to do much managing of my

portfolio is much better than having the cash sitting in the bank or having a

stranger 'manage' my investment capital with dubious results.

Self-learning

on Passive Investing

Do be careful and learn any

investment strategy well, to know the pros and cons and whether the risk and

returns meets your investment objective. Good thing is passive investing does

not need much talent to learn and implement. If you wish to learn more about

passive investing, do read on.

To start off your learning, read this

to know what a basic passive portfolio investing is about:

This is basic stock index ETF+bond

passive portfolio - personally i think this portfolio is ok and is simple to

implement, though IMO this 2 assets is not diversified enough for me.

Next, read this about more

diversified passive portfolio using Permanent Portfolio Strategy:

This uses 3 highly volatile

assets'stock index ETF, long govt bond, gold' and low volatility cash to create

a overall low volatility portfolio. You have to learn about why people such as

fund managers invest in govt. bonds and gold, in order to have confidence to

invest with Permanent Portfolio strategy. As the saying goes, do not invest in

something you do not understand. I'll admit long bond and gold may take people

mroe time to learn and use comfortably, though the rewards of understanding how

these 2 assets can be used is probably worthed it.

Then you can go explore this blog

for ideas about local implementation of Permanent Portfolio passive portfolio:

PP strategy is also widely explained

in the Internet.

Which ever passive portfolio

strategy you use is up to your comfort level. The main things about passive

investing is choosing asset allocation, yearly rebalancing and keeping long

term running cost low.

Advantages

of Passive Portfolio

I will highlight advantages of

passive portfolio here:

-No need to monitor portfolio

consistently, or pick stocks, or market time entries and exit - this removes a

lot of human errors.

-Lower maximum potential loss in

major market downturn, due to bonds prices rising during stock market

downturns.

-Near market bottom, there is

potential to sell off bonds that are doing well to buy cheap stocks in larger

quantity.

-Force investor to be contrarian and

buy assets when they are cheap and sell expensive asset to realise profits. Eg.

buy cheap bonds when stocks are going up, buy cheap stocks when stocks has had

a bad year.

-Long term returns of passive

portfolio is similar to that of pure stock index ETF.

-Stock/bond portfolio has lower risk

compared to pure equity portfolio.

-Aim of passive portfolio is for

reasonable 'market returns', not for 'beating the market'. IMO, in general,

expected long term returns for a passive portfolio should be around 7%~10% per

year.

Cons of passive investing strategy?

-When stocks prices are soaring in

bull markets and people with pure stock portfolio are saying how they are

making above 40% returns, passive portfolio with its decreasing bond prices

will make less returns at say 20% only - so no bragging rights of very high

wins for passive portfolio holders. IMO this is not a disadvantage, because the

maximum loss and gains of passive portfolio are both lesser. So passive

portfolio holders suffer less and are more likely to stick with their passive

strategy during market downturns.

Effects

of Big Capital Losses

Regarding stock market losses, I

will quote from this article:

"If you are to look back at

past trading trends, you would realize that in a bear market, stock markets

typically fall by over 50%. In Singapore, the STI fell from 2,500 points in

1996 to just 800 points in 1998, representing a 68% fall. In 2000, STI fell

from 2,500 points to 1,200 points in March 2003, representing a 52% drop. And

in 2007, STI fell 62% from 3,900 points to its lowest of 1,456 points in March

2009."

Seems like recessions can happen 2

to 4 years after the last recession has ended? I am not predicting that we are

due for a recession in 2013, and I am not saying that the stock market will be

in a 10 year bull run till 2019. I cannot predict market future like that, and

most people cannot predict market conditions in future accurately and

consistently also. I can only say with confidence that each investor will meet

with severe recession eventually and each investor is better off having a

simple workable contingency plan to avoid losses and preserve capital during

economic downturns.

During such recessions as described

above, will you stick with your investing strategy when stock markets just keep

on dropping towards -10%, -20%, -30%, -40%, -50% or more? Note that in these

recessions, your job security in that job you love may be threatened, or you

may have suffered a pay cut or retrenchment, or someone in the household may

have lost job and you have to pay for more of the bills. In such low moody and

unsure environment, how many percent of paper loss in your investment do you

think you can mentally take before deciding to cut loss and preserve your

capital to tide over the crisis? Not to mention, possibly seeing your 40% paper

profit in shares becoming -20% loss or so is such a demoralising event.

Ultimate Passive Investment

Aims

In passive investing, the one of the ultimate

aim is to preserve capital and not lose too much when market is bad. When your

losses are smaller during recessions, in the subsequent recovery period you

need less profit in order to recover the loss. Take for example an investor in

pure equity took a 50% loss during recession - subsequently he had a 60% profit

in the post recession recovery period. Did he do well enough? Not really:

(100-50)*1.6=.80%, meaning, he still suffer -20% loss even after having a fantastic

60% gain. Now look at a passive portfolio investor owning bonds in the

portfolio. During recession, perhaps the portfolio went down by 20%, and in

subsequent post recession recovery period, his investment gained 30% only. How

has this passive investor done? (100-20)*1.3=104%. This passive investor has

managed to recover his portfolio more quickly and completely during the post

recession recovery period of high stock growth.

Therefore, a pure equity investor had to endure large paper

losses during recessions, or else market time to get out before recession and

get back in after recession, while noting psychology plays big part in market

timing and most people cannot market time correctly. On the other hand, a

passive investor can ride out the economic turmoil more calmly knowing the

portfolio strategy is on the investor's side to reduce volatility, preserve

capital, and allows disciplined investing. So the lack of very high rewards and

corresponding lack very high risk in passive portfolio is actually an advantage

from several different perspectives.

Friday, 7 September 2012

Letting investment portfolio go untouched for 10 Years

Hmm..I'd explore the possibility of letting an investment portfolio go untouched for 10 years. I am a passive portfolio investor using Permanent Portfolio investing strategy, which is investing in diversified portfolio of stock index, govt long bond, gold and cash, all in equal 25% split. Rebalancing back to 25% is done every year.

1. Using figures from the 9 year chart on my blog post:

http://singapore-permanent-portfolio.blogspot.sg/2012/07/how-has-singapore-permanent-portfolio.html

I constructed following scenario: Start Permanent Portfolio in Jan 2003, and see what is the result 9 years later on Jan 2012 if portfolio is left untouched throughout 9 years.

This shows in 9 years from Jan 2003 till Jan 2012, the unmanaged portfolio will have generated 85% returns and beating inflations. 85% is before dividends and interest. It survived a major recession and some inflation along the way.

This shows in 9 years from Jan 2003 till Jan 2012, the unmanaged portfolio will have generated 85% returns and beating inflations. 85% is before dividends and interest. It survived a major recession and some inflation along the way.

The above portfolio is started with following assets in Jan 2003:

25% Singapore STI stock market index (or theoretical STI ETF),

25% TLT (iShares Barclays 20+ Yr Treas.Bond ETF), price converted to SGD,

25% gold - price converted to SGD,

25% cash - assume no bank/FD interest, for simplicity of calculation.

2. The second scenario is when investor picked the height of stock market on Jan 2008 to start a Permanent Portfolio, experienced the major recession from Jan 2008 to Jan 2009, and see how portfolio performs to date on Jan 2012, without any management for the 4 years:

This shows from Jan 2008 till Jan 2012, the portfolio survived a major recession relatively unscathed with only -4% returns, and returned total 14% four years later in Jan 2012, possibly matching inflation rate if inflation rate had been 3.5% anually

This shows from Jan 2008 till Jan 2012, the portfolio survived a major recession relatively unscathed with only -4% returns, and returned total 14% four years later in Jan 2012, possibly matching inflation rate if inflation rate had been 3.5% anually

.

This unmanaged portfolio returns is possible due to effective diversification of portfolio assets. Stock, govt long bond, gold, and cash have low or negative correlations, and together, they react dynamically to the 4 economic cycles of growth, recession, deflation, and inflation to produce overall portfolio growth through time. Each of stock, govt long bond (20~30yrs), and gold have similar high volatility, and would perform well in their preferred cycle to shoulder up the portfolio when the other assets may be dropping. Also, when starting portfolio, if one asset is very expensive, one of the other asset will likely be very cheap - so through time, the rising cheap asset will offset the droppig expensive asset.

Permanent Portfolio is normally rebalanced yearly. The above scenario serves as an interesting exercise to see if Permanent Portfolio would survive for long time if left unmanaged. The simulation results suggests that theoretically and practically, Permanent Portfolio investment strategy can provide returns if left unmanaged for long period of time. This is of course precluding rare extreme events such as hyperinflation and 20 years secular bear market in stocks. That said, even in such extreme events as hyperinflationa and 20 year secular bear market, damage to portfolio will likely be limited and portfolio will still have some remaining value due to diversification.

So, any investor planning to go on a 10-year vacation yet? :)

1. Using figures from the 9 year chart on my blog post:

http://singapore-permanent-portfolio.blogspot.sg/2012/07/how-has-singapore-permanent-portfolio.html

I constructed following scenario: Start Permanent Portfolio in Jan 2003, and see what is the result 9 years later on Jan 2012 if portfolio is left untouched throughout 9 years.

The above portfolio is started with following assets in Jan 2003:

25% Singapore STI stock market index (or theoretical STI ETF),

25% TLT (iShares Barclays 20+ Yr Treas.Bond ETF), price converted to SGD,

25% gold - price converted to SGD,

25% cash - assume no bank/FD interest, for simplicity of calculation.

2. The second scenario is when investor picked the height of stock market on Jan 2008 to start a Permanent Portfolio, experienced the major recession from Jan 2008 to Jan 2009, and see how portfolio performs to date on Jan 2012, without any management for the 4 years:

.

This unmanaged portfolio returns is possible due to effective diversification of portfolio assets. Stock, govt long bond, gold, and cash have low or negative correlations, and together, they react dynamically to the 4 economic cycles of growth, recession, deflation, and inflation to produce overall portfolio growth through time. Each of stock, govt long bond (20~30yrs), and gold have similar high volatility, and would perform well in their preferred cycle to shoulder up the portfolio when the other assets may be dropping. Also, when starting portfolio, if one asset is very expensive, one of the other asset will likely be very cheap - so through time, the rising cheap asset will offset the droppig expensive asset.

Permanent Portfolio is normally rebalanced yearly. The above scenario serves as an interesting exercise to see if Permanent Portfolio would survive for long time if left unmanaged. The simulation results suggests that theoretically and practically, Permanent Portfolio investment strategy can provide returns if left unmanaged for long period of time. This is of course precluding rare extreme events such as hyperinflation and 20 years secular bear market in stocks. That said, even in such extreme events as hyperinflationa and 20 year secular bear market, damage to portfolio will likely be limited and portfolio will still have some remaining value due to diversification.

So, any investor planning to go on a 10-year vacation yet? :)

Tuesday, 28 August 2012

What to invest in to start Singapore Permanent Portfolio

What to invest in to start Singapore Permanent Portfolio?

(updated 2/3/2013)

Following is an example plan to show how an investor can start a Singapore Permanent Portfolio. The figures here are for readers to double check against the figures in their own plans to start a Singapore Permanent Portfolio, and are not advices nor recommendations that readers should invest in these particular assets. In the example, an investor starts with minimum sum S$12,000. The investor strives to get as close to 25% initial allocation for each asset as possible. Below figures exclude brokerage fees and annual fees.

Example: Using data from 2 April 2012, to start a Singapore Permanent Portfolio, an investor can invest about S$12,000 all at once in:

25% Stocks: (updated 2/3/2013)

i.1 lot (1000 shares) of SPDR STI ETF (SGX symbol ES3) at S$3.04 per share - total investment S$3040. ES3 is traded in individual board lot of 1000 shares each.

ii. Alternatively, invest 10 lots (1000 shares) of Nikko AM STI ETF100 (SGX symbol G3B) at S$3.04 per share - total investment S$3040. G3B is traded in individual board lot of 100 shares each.

25% Bonds: (updated 30/8/2013)

i. 3 lots (30 units) of Singapore Government 30-year Bond (SGX symbol PH1S) at S$100.0 per unit - total investment S$3000. PH1S is traded in individual board lot of 10 units each.

Note: 30 years bonds are to be held till they are left with near 20 years left till maturity, then the bonds are all sold and newer 30 years bonds, or near 30 years bonds, are bought in replacement. This is to ensure the bonds will always have a "long" time till maturity in order to keep the volatility of the bonds prices high. This also mean that the 30 years bond will never be held till 'maturity'.

(With effect from 1 April 2013, CDP will remove the administrative fees of 0.08% (8 basis points) of the face value of the SGS per annum.)

25% Gold:

i. Invest 1 lot (10 share) of SPDR Gold Shares GLD ETF 10US$ (SGX symbol O87) at US$161.48 per share - total investment US$1614.80 or S$2023 (USDSGD 1.25293). O87 is traded in individual board lot of 10 units each.

ii. Alternatively, invest 45 grams of gold in UOB Gold Savings Account at S$67.45 per gram (S$2098 per ounce) – total investment S$3035.25 - note that that will incur 1.54 grams (include GST 7%) per year or 3% annual fees, so Gold Savings Account is not advisable for S$3000 investment. At gold price of S$67.45 per gram, investing S$20,000~S$25,000 will incur annual fees of 0.49%~0.39% which is about equivalent to annual fees of GLD ETF. To achieve minimal annual fees of 0.25% from Gold Savings Account, S$38,850 of investment is needed.

iii. For gold investments, there is no need to hedge the gold value back to SGD, irregardless of which currency the gold is bought in - this allows gold to do its job as an inflation protection hard asset against core inflation and SGD devaluation.

iv. Calculate your latest returns on gold in SGD here: http://goldprice.org/Calculators/Gold-Price-Calculators.html

25% Cash: (updated 5/2/2017)

i. Deposit about S$3000 in Philip Money Market Fund. This can be done by depositing the cash into Phillip Cash Management Account by ATMs or internet banking, using Electronic Payment of Shares (EPS) Lump Sum Payment option, or by Online Bill Payment option. Any cash left in the Phillip Cash Management Account will be automatically invested into the Phillip Money Market Fund at no extra charge. Cash can be deposited and withdrawn from Phillip Cash Management Account within one working day.

ii.Alternatively, invest into 2 lots (200 shares) of iShares Barclays Asia Local Currency 1-3 Year Bond Index ETF (SGD) (This ETF holds sovereign bonds only, SGX symbol QL0 "zero") at S$12.62 per share - total investment is S$2524, while remainin S$476 goes into Money Market Fund if possible. QL0 is traded at individual board lots of 100 shares each. Investing in short term bonds is still subjected to some forex and interest rate risk, so make sure investor has sufficient cash for living or emergency use to minimise the need to sell this short term bond ETF for liquid cash. (Investing in short term bond fund is not proven replacement for cash component... invest at own discretion.)

iii. Alternatively, invest S$3000 in 1-year Singapore Treasury Bill – total investment S$3000. Singapore T-bill is a fully 'insured' asset as the Singapore government fully backs the Singapore Treasury Bill.For Singapore Treasury Bill, there is a CDP administrative fees of 0.04% or minimum S$1.50 to be deducted every half yearly during interest payment.

(With effect from 1 April 2013, CDP will remove the administrative fees of 0.08% (8 basis points) of the face value of the SGS per annum.)

iv. (Best Option) Alternatively, invest S$3000 in Singapore Savings Bond (SSB). Unique features: Maximum 10 years term - able to do early redemption in any month before the bond matures, with no penalty for exiting the investment early. Meaning, accumulated interest on the redemption amount shall be paid, together with 100% of your initial investment. Interest rate increases every year, so the longer you hold the Savings Bond, the more annual interest you receive. Criteria to invest this Savings Bond: a. A bank account with DBS/POSB, OCBC or UOB; b. An individual CDP Securities account linked to any of your bank accounts; c. Apply through ATMs or Internet Banking. Savings Bond is issued every month, and total amount of Savings Bonds held across all issues cannot be more than $100,000.

Rebalancing - Managing Portfolio: After starting the Permanent Portfolio fund, the investor does not need to monitor the portfolio frequently. The only time to manage the portfolio is during rebalancing event. Rebalancing can happen in 3 ways.

An investor should understand and plan their investment strategy well, including reasons for asset allocations, how and when to rebalancing portfolio, and the benefits and disadvantages of a particular portfolio strategy. An example of a well designed investment portfolio strategy is the Permanent Portfolio strategy, and detailed description of Singapore Permanent Portfolio investment strategy can be found on this website.

(updated 2/3/2013)

Following is an example plan to show how an investor can start a Singapore Permanent Portfolio. The figures here are for readers to double check against the figures in their own plans to start a Singapore Permanent Portfolio, and are not advices nor recommendations that readers should invest in these particular assets. In the example, an investor starts with minimum sum S$12,000. The investor strives to get as close to 25% initial allocation for each asset as possible. Below figures exclude brokerage fees and annual fees.

Example: Using data from 2 April 2012, to start a Singapore Permanent Portfolio, an investor can invest about S$12,000 all at once in:

25% Stocks: (updated 2/3/2013)

i.1 lot (1000 shares) of SPDR STI ETF (SGX symbol ES3) at S$3.04 per share - total investment S$3040. ES3 is traded in individual board lot of 1000 shares each.

ii. Alternatively, invest 10 lots (1000 shares) of Nikko AM STI ETF100 (SGX symbol G3B) at S$3.04 per share - total investment S$3040. G3B is traded in individual board lot of 100 shares each.

25% Bonds: (updated 30/8/2013)

i. 3 lots (30 units) of Singapore Government 30-year Bond (SGX symbol PH1S) at S$100.0 per unit - total investment S$3000. PH1S is traded in individual board lot of 10 units each.

Note: 30 years bonds are to be held till they are left with near 20 years left till maturity, then the bonds are all sold and newer 30 years bonds, or near 30 years bonds, are bought in replacement. This is to ensure the bonds will always have a "long" time till maturity in order to keep the volatility of the bonds prices high. This also mean that the 30 years bond will never be held till 'maturity'.

(With effect from 1 April 2013, CDP will remove the administrative fees of 0.08% (8 basis points) of the face value of the SGS per annum.)

25% Gold:

i. Invest 1 lot (10 share) of SPDR Gold Shares GLD ETF 10US$ (SGX symbol O87) at US$161.48 per share - total investment US$1614.80 or S$2023 (USDSGD 1.25293). O87 is traded in individual board lot of 10 units each.

ii. Alternatively, invest 45 grams of gold in UOB Gold Savings Account at S$67.45 per gram (S$2098 per ounce) – total investment S$3035.25 - note that that will incur 1.54 grams (include GST 7%) per year or 3% annual fees, so Gold Savings Account is not advisable for S$3000 investment. At gold price of S$67.45 per gram, investing S$20,000~S$25,000 will incur annual fees of 0.49%~0.39% which is about equivalent to annual fees of GLD ETF. To achieve minimal annual fees of 0.25% from Gold Savings Account, S$38,850 of investment is needed.

iii. For gold investments, there is no need to hedge the gold value back to SGD, irregardless of which currency the gold is bought in - this allows gold to do its job as an inflation protection hard asset against core inflation and SGD devaluation.

iv. Calculate your latest returns on gold in SGD here: http://goldprice.org/Calculators/Gold-Price-Calculators.html

25% Cash: (updated 5/2/2017)

i. Deposit about S$3000 in Philip Money Market Fund. This can be done by depositing the cash into Phillip Cash Management Account by ATMs or internet banking, using Electronic Payment of Shares (EPS) Lump Sum Payment option, or by Online Bill Payment option. Any cash left in the Phillip Cash Management Account will be automatically invested into the Phillip Money Market Fund at no extra charge. Cash can be deposited and withdrawn from Phillip Cash Management Account within one working day.

ii.

iii. Alternatively, invest S$3000 in 1-year Singapore Treasury Bill – total investment S$3000. Singapore T-bill is a fully 'insured' asset as the Singapore government fully backs the Singapore Treasury Bill.

(With effect from 1 April 2013, CDP will remove the administrative fees of 0.08% (8 basis points) of the face value of the SGS per annum.)

iv. (Best Option) Alternatively, invest S$3000 in Singapore Savings Bond (SSB). Unique features: Maximum 10 years term - able to do early redemption in any month before the bond matures, with no penalty for exiting the investment early. Meaning, accumulated interest on the redemption amount shall be paid, together with 100% of your initial investment. Interest rate increases every year, so the longer you hold the Savings Bond, the more annual interest you receive. Criteria to invest this Savings Bond: a. A bank account with DBS/POSB, OCBC or UOB; b. An individual CDP Securities account linked to any of your bank accounts; c. Apply through ATMs or Internet Banking. Savings Bond is issued every month, and total amount of Savings Bonds held across all issues cannot be more than $100,000.

Rebalancing - Managing Portfolio: After starting the Permanent Portfolio fund, the investor does not need to monitor the portfolio frequently. The only time to manage the portfolio is during rebalancing event. Rebalancing can happen in 3 ways.

- In first method, the investor will leave the portfolio alone untouched, until one of the asset reaches 35% or 15% of portfolio, in which case the portfolio will be rebalanced back to 25% equal spilt among the 4 assets - this rebalancing band method is to be used when there will be no fresh fund entering portfolio, and aims to follow momentum of portfolio and let profits run.

- For second method, if there is fresh fund to put into portfolio, the fresh fund will usually buy into the worst performing asset at every year end, or at regular monthly or quarterly interval, so that each asset becomes 25% of portfolio again - this is to reset the risk/reward ratio of the portfolio and buy assets when they are cheap.

- The third method of rebalancing is to use fresh fund to buy into different assets, while keeping the asset ratio unchanged - this aim to let profits run and to only rebalance when one of the asset reaches 35% or 15% of portfolio.

An investor should understand and plan their investment strategy well, including reasons for asset allocations, how and when to rebalancing portfolio, and the benefits and disadvantages of a particular portfolio strategy. An example of a well designed investment portfolio strategy is the Permanent Portfolio strategy, and detailed description of Singapore Permanent Portfolio investment strategy can be found on this website.

Monday, 30 July 2012

How do I keep track of Permanent Portfolio performance

How do I

keep track of Permanent Portfolio performance?

ES3.SI is the Yahoo! Finance symbol for STI ETF (ES3) that trades on Singapore Stock Exchange.

I use Android app Stock Watcher to watch my Singapore Permanent

Portfolio performance. Warning: looking at the portfolio frequently can induce

anxiety or happiness according to the day’s market situation! It is advisable

to look at the portfolio performance less frequently, preferably once a year, once

a quarter or when market seems likely to make major moves that would cause one

of your asset to rise or drop by 40% or more, which is when it would likely

cause the 15% or 35% rebalance band to be hit. According to my research with available data, after the portfolio is started or rebalanced, it may take minimum one to three months before the portfolio starts to show consistent positive profits, if any. A good thing is that Permanent Portfolio volatility is not so high so any drop in total portfolio value looks more bearable.

Explanation:ES3.SI is the Yahoo! Finance symbol for STI ETF (ES3) that trades on Singapore Stock Exchange.

PH1S.SI is the

Yahoo! Finance symbol for Singapore Government 30-year bond (PH1S) that trades

on Singapore Stock Exchange.

XAUSGD=X is the

Yahoo! Finance symbol for price of gold in Singapore dollars. Whether I invest

in UOB Gold savings account (which counts gold in grams instead of ounce), or

whether I bought gold ETF (O87) in US dollars, I would find the equivalent Singapore

dollar spot gold price (XAUSGD) at the time of purchase and use it as the buy

price of my gold. This way I can use XAUSGD to directly evaluate the

performance of gold investment in my local country currency.

A screen shot example of how the Stock Watcher app is setup here. This app shows

an example Permanent Portfolio started on 4 April 2012 with the price of ES3, PH1S and

XAUSGD on that day and the current performance. For a more complete view of the portfolio performance, I keep track of portfolio results including cash performance manually in a spreadsheet.

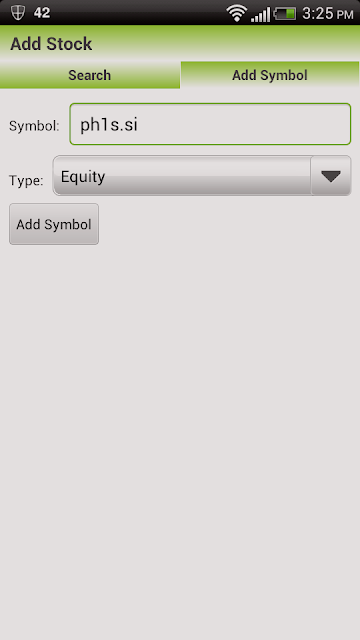

To add 'PH1S.SI' and 'XAUSGD=X' symbols to the 'Portfolio' tab:

Under [Portfolio] tab,

-> press the phone's [menu] button

-> select [Add] button

-> select [Add Symbol] tab

-> key in 'ph1s.si' and press [Add Symbol] button. Do the same for 'xausgd=x'.

-> press the phone's [menu] button

-> select [Add] button

-> select [Add Symbol] tab

-> key in 'ph1s.si' and press [Add Symbol] button. Do the same for 'xausgd=x'.

See picture example below:

Subscribe to:

Posts (Atom)